How Latin America Is Finding Its Path to Economic Prosperity Again

A Just Transition as the target

SWP Comment 2023/C 21, 03.04.2023, 6 Seitendoi:10.18449/2023C21

ForschungsgebieteThe traditional image of Latin America as a troubled region seems to continue even after the Covid-19 crisis, this time in the wake of the war in Ukraine and the sanctions imposed by the West. Inflationary pressures, budget deficits and the danger that broad sections of the population will slip into poverty are fuelling negative scenarios. There are initial indications that some countries are already experiencing payment difficulties. Demands from Latin American governments for debt relief or the renegotiation of foreign debt are being put on the agenda as part of a reorientation of the development model towards sustainability and climate protection criteria. This requires a far-reaching structural change, away from the traditional commodity-based economies and towards an environmentally and socially compatible development path. Germany and Europe must also shift course by contributing to the conservation of natural resources and not just to their exploitation.

The complex economic situation in Latin American and Caribbean (LAC) countries with inflation, rising debt and the tendency to devalue national currencies brings back bad memories in the region. A relapse into macro-economic instability is to be absolutely avoided. By raising interest rates and maintaining high foreign exchange reserves, governments are attempting to ward off the dangers threatening currency stability as a result of uncertainty on the international markets. The aim is to create stable macro-economic conditions. Governments are also trying to mitigate the effects of the economic crisis with subsidies for transport, energy and food prices, sales tax cuts for price-sensitive products and selective price controls. Once more, many countries are relying on export growth to overcome the crisis. However, there are only limited opportunities for it at present. Global demand indicators do not point in this direction. Even if there were a boom in demand, the desired effect might not materialise due to the limited possibilities for quickly expanding production.

China is again emerging as an alternative partner: Most countries in Latin America and the Caribbean cannot afford to lose the Chinese market and the investments coming from there. China has offered long-term credit facilities in the past. These saved the LAC countries from having to ask for bridging loans from international financial organisations such as the International Monetary Fund (IMF) and the World Bank, which come with stringent requirements and conditionalities. In this way, it was possible for Chinese companies to secure market entry. When payment difficulties arose, for example in the debtor countries Venezuela, Argentina and Ecuador, Beijing granted payment deferments and arranged talks on restructuring options. This approach was perceived in the region as a long-term strategy (“patient capital”), although the Chinese lenders allowed themselves to be contractually placed at the top of the repayment list in case of a potential default.

But resorting to other sources of finance is not the only instrument in crisis management. Governments seek to avoid regional contagion effects. These can occur if all countries reduce their spending at the same time, causing demand to collapse in other countries as well. Governments also try to minimise their vulnerability to financial crises by increasing their export revenues. The easy path back to the commodity economy is thereby mapped out. However, there is a growing resistance to this established pattern of crisis management emerging in the region.

Another lost decade for Latin America?

Due to the Covid-19 pandemic and intensified economic and social challenges, the development of the subcontinent has been set back many years. The already weak democratic institutions have suffered further damage, the level of distrust in institutions has increased, and political and social consensus is eroding. Not without reason has there been talk of a “new lost decade” in Latin America. This refers to the long shadow of the Latin American debt crisis in the 1980s. During this period, the countries of the region reached a point where their external debt was far higher than the strength of their economies. Because they had been living beyond their means, they suffered a massive loss of wealth and a spike in poverty rates, which significantly affected their development.

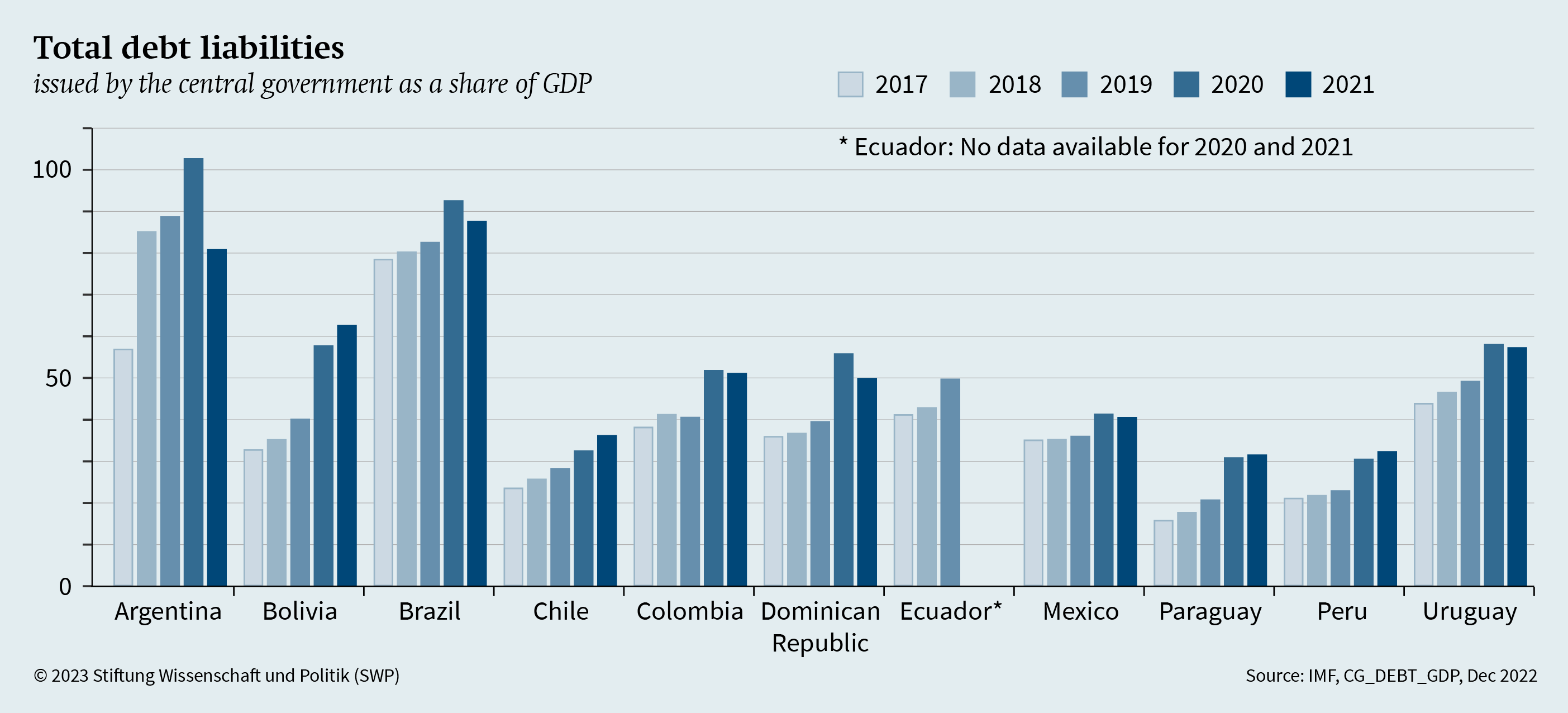

A similar dynamic is feared again today, given the significantly flattened growth curve, inflation pressures and the difficulties of some countries such as Argentina, Suriname and Ecuador to meet their payment obligations. Annual economic growth in the region from 2014 to 2023 averaged 0.9 per cent, half that of the “lost decade”. Although debt servicing in the region as a whole has not yet reached threatening dimensions, existing or emerging financial constraints cannot be ignored for small states such as Belize, Jamaica, Barbados, Guyana, Suriname and Panama. Internationally supported “buy-backs” could be a helpful remedy, whereby public funds are used to buy back – and subsequently cancel – the debts of crisis countries far below their nominal value.

In the short to medium term, the prospects for economic development in Latin America are only modest. The economic recovery following the Covid-19 pandemic has lost momentum. Now the growth rates of the LAC economies have fallen back, averaging 0.3 per cent per year in the crisis years 2014 to 2019. As a result, per capita income has shrank. According to projections by the World Bank, economic growth in the region will slow to 1.3 per cent in 2023 compared to 3.6 per cent the year before, and it will only regain momentum in the coming years. However, if domestic demand is dampened by inflation-related punitive monetary policies, this may suppress economic development more than expected. If export prices for raw materials fall significantly as a result of decreasing global demand and worsening conditions on the international financial markets, there is a growing danger that currencies will be devalued and external capital will run off. This would have a negative impact on the balance of payments. Bolivia has already had to fall back on its special drawing rights with the IMF to obtain additional liquidity to support the fixed exchange rate of the boliviano against the US dollar.

|

Figure

|

|

Source: International Monetary Fund, Global Debt Database, Central Government Debt, December 2022, https://www.imf.org/external/datamapper/CG_DEBT_GDP@GDD/SWE |

It is therefore not only in this Andean country that higher levels of poverty and inequality are to be feared. Both are expected to grow further in the region by the end of 2023, mainly due to the economic slowdown and rising inflation, especially of food prices, which hits the poorest particularly hard. Inflationary pressures are squeezing social welfare systems financially, which will inevitably lead to disputes about how to cushion the consequences of the crisis. With increasing fiscal budget constraints, energy and food subsidies as well as direct transfers for the weakest sectors of LAC societies will become necessary in order to prevent a slide into even greater poverty. If the political instability in countries such as Argentina and Brazil persists and the standards of living of large population groups stagnate or decline, there is the threat of renewed social unrest with strikes and production restrictions. In addition, the perception of many people that they have only limited or no economic opportunities forms the breeding ground for continuing violence and endemic corruption.

Therefore, suitable instruments must be considered to remedy these shortcomings. It is a matter of setting in motion debt relief and at the same time cushioning the negative effects of existing financing gaps with the help of risk-hedged credit facilities (for example against exchange rate fluctuations). With the exception of countries such as Cuba and Venezuela, which are operating outside the international capital markets, efforts are needed that are tailor-made for the special needs of middle-income countries. These include the majority of territories in the LAC region. It is important to counteract the recurring economic crises and the tendency for all measures to have a pro-cyclical effect, thereby exacerbating the downturn. The emerging liquidity problems must be prevented using debt deferrals and extensions. The United Nations Economic Commission for Latin America and the Caribbean (ECLAC/CEPAL) fears that increased social policy expenditures in important countries could further reduce fiscal space. Therefore, the Commission strongly warns against premature fiscal adjustments, as they could stifle weak growth impulses and derail development efforts. Ultimately, the accumulation of large foreign exchange reserves in order to protect against external shocks and ensure national currency stability can only be achieved at the expense of economic growth, as the Mexican example shows.

Joint action against inflationary pressures in the region

The left-oriented governments of the region see considerable potential for social unrest with rising or high-level inflation. Therefore, they are striving to take joint measures to curb currency devaluations and establish food security. The presidents of Argentina, Brazil, Mexico, Colombia and Cuba are trying to establish an “anti-inflation front in Latin America” to control the prices of essential goods in their countries, either by lowering import tariffs or by giving the respective partner countries preferential access to each other. The aim is to establish an intergovernmental trade partnership that Bolivia, Chile and Honduras could also join. The exchange of goods between countries should be organised in such a way that higher prices among the countries are offset with supplies. This would require the active participation of manufacturers, intermediaries and consumers. However, such a procedure would only be feasible if it does not involve products for which these countries are in competition with each other. This pattern of solidarity and reciprocal aid is expected to succeed in bringing down inflation and relieving the burden on consumers, especially those in the poorest sectors. Especially for Argentina with an inflation rate of 95.2 per cent, Colombia with 13.1 per cent and Cuba with 39.7 per cent (each in 2022), such an option is an additional lifeline in the face of rising food prices.

In October 2022, the Mexican government had already agreed with 15 producers and supermarket chains on a national regulation for 24 basic food products. To this end, it suspended bureaucratic barriers to imports, distribution and further processing of the intended products. At the same time, it imposed an export ban on certain strategic goods in order to safeguard national production. With the help of this agreement, the costs of the 24 products are to be reduced by 8 percent for consumers. In addition, fertilisers are to be supplied at preferential prices or even free of charge.

It is questionable, however, how effective the ways of controlling inflation envisaged in both the national and regional frameworks will be. On the one hand, price dynamics are largely due to the international impact of the war in Ukraine. On the other hand, price controls put pressure on public budgets when, for example, the taxation of fuel in Mexico is suspended or certain farms are supplied with fertiliser free of charge. It is therefore feared that the plan of a common front against inflation will primarily serve the governments’ interests in demonstrating their capacity to act, without the desired long-term effects.

Combining energy transition, climate change and debt relief

After years of widespread crisis experience, the countries of the region are still facing enormous challenges. In the short term, the aim is to make the economies of these countries resilient, for example by combating inflationary trends and restoring fiscal capacities in the face of empty public coffers. In the medium term, it is important to promote a new energy and production matrix and the creation of high-quality jobs in the formal sectors. However, the timeline for achieving these targets continues to falter, as the turmoil of the Ukraine war and the sanctions policies of the West have placed additional burdens on the economies. These include price increases for strategic goods (fertilisers) and food, production losses as a result of interrupted supply chains and delivery shortages.

Despite this complex situation, a debate is currently underway in Latin America and the Caribbean on how this comprehensive economic and policy agenda can be linked to the region’s natural and energy capital in a way that generates innovative industrial policy drivers. The aim is to value this capital in a way that promotes productivity growth and supports the development of new “green economy” industries. Such a transition requires a particularly high level of political decision-making power in a region that is rich in raw materials, as it requires the mobilisation of substantial financial resources that have so far been generated primarily through raw material exports.

The tendency to emerge from the crisis in the traditional role of an exporter of raw materials is just as present in the LAC debate as the interest to set a new course, that is, shifting towards more comprehensive value creation through the further processing of raw materials in one’s own country or in the region. Therefore, it is expected that there will be difficult and conflict-ridden processes of social understanding concerning these goals. Initial steps have already been taken in Chile and Colombia, which can serve as showcases for the complex processes of understanding and agreement between social forces and interest groups. Since many countries continue to live on oil revenues – Argentina, Brazil, Ecuador, Mexico, Peru, Guyana, Trinidad and Tobago, Venezuela – there is a great path dependency that will require considerable efforts to overcome. The shift away from fossil fuels and the decarbonisation of the national energy matrix can hardly be achieved by governments without broad national support and the corresponding investment of capital.

As a springboard for this change, the region has a strategic position, as it can use and supply important minerals for the energy transition. In 2017, Latin America and the Caribbean held 61 per cent of the world’s lithium, 39 per cent of its copper and 32 per cent of its nickel and silver reserves. Today, it no longer makes sense for governments in Chile, Colombia and other countries to meet only the international demand for these raw materials. They want to fundamentally reshape their production profiles, which means nothing less than an economic and political reversal: New industrial policy drivers must be set to leave the old pattern of commodity-exporting economies behind. Against the backdrop of restrictive international monetary policies and reduced capital flows to the region, tax policy measures are also needed to cover the necessary capital requirements. In addition, national and multilateral development banks and the private sector are being called upon to mobilise investment capital with favourable conditions.

The aim: A Just Transition

The normative horizon of a socially acceptable and Just Transition to a sustainable economy is firmly anchored in the development debate. The main aim is to ensure social resilience in the respective societies and to avoid the distortions that a change in the development path towards sustainability could bring.

However, when thinking about the energy transition, climate change and debt policy together also point to a variety of conflicting goals: There is no patent remedy for a Just Transition; the concrete form it takes must be adapted to local conditions. Specific approaches are needed for the respective contexts, which are often not in line with the general principles of development cooperation. Side-effects can become significant obstacles: In Mexico and Brazil, wind farms have met with resistance from rural communities, who sue for consultations before the turbines are built. In Ecuador, the demand for balsa wood – one of the most important materials for building wind turbine blades – has increased pressure on forests in the Amazonas region. In Argentina, thousands of people follow the call of “fossil energy” to the oil industry in Vaca Muerta in search of jobs. This geological formation stretches across several provinces and contains some of the world’s largest shale gas reserves.

Such distortions must be addressed by Germany’s and Europe’s development cooperation. However, the weaknesses of LAC production chains and their laxer environmental and labour standards have made it difficult to conclude trade agreements such as the Mercosur-EU (European Union) agreement. Increasingly, voices from the region are expressing concerns about possible “green” protectionism and encroaching extra-territorial regulations that the EU could impose through its principles and standards, such as the European regulation on deforestation and forest degradation. This argument – which is also referred to as “regulatory imperialism” – should not be underestimated, as it follows on from the argument against European partners that they defend market protectionist interests with environmental justifications. The more the global energy transition takes hold, the more new geopolitical alliances and rivalries will emerge that need to be managed.

In order to avoid or mitigate as many of these as possible, the member states of the EU should work together with the countries of the region to develop shared standards. In this way, they would help to ensure that elements of the Escazú Agreement (see SWP Comment 4/2021) also become part of the European rules and that a process for the mutual development of standards and procedures begins. In this way, it may be possible to escape from the winner–loser logic that is likely to take hold in view of the massive international shifts during the course of the energy transition. Germany and Europe should support the formulation of a targeted industrial policy in the LAC countries and help close the existing funding gaps for the Just Transition. This means, on the one hand, converting the debt and orienting themselves towards the Just Transition target, knowing full well that even the middle-income countries in Latin America and the Caribbean are not robust enough to withstand the symptoms of the crisis. Most LAC countries do not meet the requirements for the existing debt conversion facilities. Moreover, these facilities are usually linked to prior agreements with the Paris Club, so that their impact in relieving the burden on the budget is very limited.

Debt-for-climate swaps – as a further development of the debt-for-nature swaps practised in Belize in 2021 – would be a suitable instrument to facilitate the path towards a lower-carbon economy, and at the same time create budgetary room for manoeuvre so that the LAC countries can invest in social resilience and sustainable development. However, this re-orientation will only be sustainable if much more effort is put into protecting the existing raw materials in the region, rather than establishing a new partnership between Europe and countries in Latin America and the Caribbean with an interest in their exploitation.

Further Reading

Günther Maihold, Tania Muscio Blanco and Claudia Zilla, From Common Values to Complementary Interests. For a new conception of Germany’s and the EU’s relations with Latin America and the Caribbean, SWP Comment 1/2023 (Berlin: SWP, January 2023)

Prof. Dr Günther Maihold is Deputy Director of SWP. This paper was written as part of the project “The Impact of the Ukraine War on Latin America / Caribbean and Relations with Germany and Europe”.

© Stiftung Wissenschaft und Politik, 2023

All rights reserved

This Comment reflects the author’s views.

SWP Comments are subject to internal peer review, fact-checking and copy-editing. For further information on our quality control procedures, please visit the SWP website: https://www.swp-berlin.org/en/about-swp/ quality-management-for-swp-publications/

SWP

Stiftung Wissenschaft und Politik

German Institute for International and Security Affairs

Ludwigkirchplatz 3–4

10719 Berlin

Telephone +49 30 880 07-0

Fax +49 30 880 07-100

www.swp-berlin.org

swp@swp-berlin.org

ISSN (Print) 1861-1761

ISSN (Online) 2747-5107

DOI: 10.18449/2023C21

(English version of SWP‑Aktuell 24/2023)