Dr Laura von Daniels is Head of The Americas Division at SWP.

The author gratefully acknowledges financial support from the American-German Institute (AGI) at Johns Hopkins University and the Konrad Adenauer Foundation for making it possible to participate in the seminar “Post NAFTA: US, Germany, Canada and Mexico in the Global Economy” in March 2019 in Washington, D.C. Special thanks also go to Peter Chase, Martin Chorzempa, Jonathan Hackenbroich, Harold James, Matthias Jorgensen, Cecilia Malmström, André Sapir, Peter Sparding and many other interlocutors in Berlin, Brussels, Paris and the United States who were willing to share their perspectives on the transatlantic economic relationship.

-

The United States sees the rise of authoritarian China as the primary risk to its national security and the global order.

-

US foreign policy views the economy across party lines as being part of “national security” – especially vis-à-vis China. In its competition with China, the United States is increasingly resorting to coercive economic instruments, some of which can also apply to companies in third countries. These are primarily tariffs, financial sanctions as well as export and investment controls.

-

Industrial policy, including large-scale subsidies, complements these defensive economic measures.

-

US allies and economic partners see both coercive economic measures and industrial policy as challenges.

-

Biden’s customised technology controls (“small yard, high fence” approach) are being met with scepticism concerning their scope, practicability and effectiveness.

-

Biden’s new industrial policy was seen as a risk to the economic base of the European Union and was introduced at a particularly bad time – when European industry is struggling most with energy price increases and rising production costs.

-

In this situation, the European Commission has rightly initiated a process to focus on the EU’s own vulnerabilities and to strengthen the coordination of external economic policy decision processes beyond trade policy. Regardless of the outcome of the US presidential election in 2024 – and in order to reduce dependence on an authoritarian China – the European Commission and the governments of the member states should work together with companies to further develop de-risking strategies and to control critical technologies. The Commission’s recently published package of measures on economic security is an important step in this direction.

-

The next European Commission should set up an Economic Security Council to independently assess issues relevant to the EU’s security and economy and enable faster and better informed decisions by the member states.

Table of contents

2 America First, Protectionism and Security Policy Realignment under Trump

2.1 Overview of the trade policy instruments

2.1.1 Section 201 duties (temporary relief)

2.1.2 Section 232 tariffs (national security threat)

2.1.3 Section 301 tariffs (Intervention against unfair trade practices)

2.2 Further coercive economic instruments vis-à-vis China

2.2.2 Investment controls and financial sanctions

3 Biden’s Economic Policy Concepts

3.1 Foreign policy for the middle class

3.2 Economic stability, national security and competition with China

4 Implementation of the Economic Policy Agenda

4.1 Security orientation of foreign trade policy

4.2.1 Infrastructure Investment and Jobs Act of 2021

4.2.2 Inflation Reduction Act of 2022

4.2.3 CHIPS and Science Act of 2022

4.3 Coercive measures against China

4.3.1 Continuation of punitive tariffs

4.3.3 Investment controls and financial sanctions

4.4.1 EU-US Trade and Technology Council (TTC)

4.4.2 Indo-Pacific Economic Framework for Prosperity (IPEF)

4.4.3 Further regional partnerships

4.4.4 Bilateral trade agreements

4.4.5 Multilateral trade order and WTO reform

4.4.6 Climate and trade policy

5 Outlook: Two Scenarios for a Strategic Foreign Economic Policy after the US Elections

5.1 Scenario 1: Continuation with Biden

Issues and Recommendations

The United States increasingly views the economy as part of its national security, and China is seen as the greatest threat to US national security across party lines. In order to prevent China’s rise to an economically, technologically and ultimately militarily superior power, the United States is prepared to use all available foreign policy tools. Even under President Barack Obama, there was a growing willingness to use coercive economic instruments in the competition with China to achieve technological supremacy. President Donald Trump introduced a whole range of such instruments against China. President Joe Biden held on to them and even sharpened some of them to increase their effectiveness. The US Congress also passed several resolutions and laws to tighten foreign economic policy instruments. Regardless of the outcome of the 2024 presidential election, the next US administration will maintain this course.

Trump was the first US president since Richard Nixon to bring about a 180-degree turnaround in the country’s strategic approach towards Beijing. In the US National Security Strategy (NSS) under Trump, China was declared to be the greatest foreign and security policy threat for the first time. In order to put Beijing in its place, the Trump administration used a trade policy statute from the Cold War that allowed it to take action against the theft of intellectual property with comprehensive tariffs. The tariffs imposed unilaterally by the United States provoked countermeasures and triggered a Sino-American trade conflict. Trump ultimately failed in his attempt to force China to give in and abandon its aggressive trade practices. He also failed to achieve his goal of reducing the US trade deficit in a sustainable way. Other coercive economic instruments, such as export controls, investment restrictions and sanctions, on the other hand, fundamentally changed the course towards China because they made it considerably more difficult for Beijing to access critical technologies. In doing so, Trump actively disregarded the interests of allies and partners and imposed tariffs on them as well. He later forced their companies to take measures against China. They were given a choice to either stop economic exchanges with companies or individuals targeted by US sanctions or lose access to the US market and be cut-off the US-dollar-based financial system. This provoked resistance from US allies, although in some cases their interests coincided with those of Washington.

As president, Biden has continued his predecessor’s strategic course towards China. However, Biden wanted to avoid the mistake of going it alone against America’s main strategic challenger by involving allied states in many decisions from the outset. Unlike in Trump’s NSS, both systemic competition with authoritarian China and cooperation with allies are anchored as priorities in his successor’s NSS. However, Biden’s top priority is the economic stability of the US middle class, not least to strengthen US democracy. All foreign policy measures must be geared towards this.

Biden is linking competition with China with the aim of strengthening the United States’ own economic power and democracy. To this end, the Biden administration has developed and gradually implemented the “Foreign Policy for the Middle Class” strategy. Undoubtedly, Biden has tried to protect US companies from export competition, relying on protectionist measures such as tariffs, even though numerous empirical studies show that these do not help the majority of US workers. He is sticking to import tariffs, which affect around two-thirds of the volume of imports from China – primarily in order to exert further pressure on China in terms of foreign and security policy.

Beyond coercive measures against China, Biden is focusing on advancing the US economy through a new industrial policy. In doing so, Washington is promoting areas in which dependence on other countries, above all China, has increased in recent decades. In addition, the development and production of state-of-the-art technologies is to be relocated to, or expanded in, the United States. In particular, the transfer of critical technologies to China is to be controlled and, if necessary, prevented. As the Biden administration explained, it is pursuing an approach (“small yard, high fence”) focused on individual economic sectors that does not call China’s economic growth into question. It remains to be seen to what extent this narrow approach will continue.

Independent of the 2024 presidential election outcome, the United States is unlikely to change its foreign policy course towards China. Under Trump, the US-China conflict could escalate more easily than under Biden, as there would be even fewer areas left for foreign policy cooperation. Working with China on climate policy would be almost inconceivable because the majority of Republicans reject both. Cooperation on standards for the application of artificial intelligence (AI) would also seem unlikely. Furthermore, under a Republican presidency, important progress on the reform of the World Trade Organization (WTO), such as subsidy rules or dispute settlement, would be virtually impossible.

If Trump were to return to the presidency, the European Union (EU) would once again be under pressure to comply with his demands – primarily because it is still dependent on the United States for security policy. Germany would be particularly vulnerable to Trump’s threats, such as tariffs on cars, due to the importance of the United States as an export market. It is clear that Trump would be prepared to link security guarantees with economic quid pro quos in order to advance his interests. As evidenced during his 2017–2021 presidency, attempts by individual countries to get permanent “good deals” in bilateral negotiations with Trump are usually fruitless. Making him aware of the raw economic costs of doing so may be the only way to prevent him from pulling out of Europe militarily. Investments in the United States and the economic involvement of US companies in the EU are therefore also central to alliance security. Berlin and Brussels should take this geopolitical factor into account when making decisions on industrial and investment promotion, including subsidies. The European response to Trump’s return should not be “more investment from and into China”.

Even in the event of a continued Democratic presidency, the demands from the US Congress and the public to take a firm economic stand towards Beijing are unlikely to abate. The EU and Germany must be prepared for Washington to expect more involvement from them in coercive measures against China. In order to better assess threats to the EU’s security and swiftly implement joint measures, the next European Commission should establish an Economic Security Council. At the same time, the German government should continue to support the EU’s course and not isolate itself by unilaterally pursuing German interests that contradict the positions of other member states. However, Germany should use its influence with other EU members to conclude important, long-term trade agreements as quickly as possible, thus underpinning the “openness” in the EU’s “open strategic autonomy”.

America First, Protectionism and Security Policy Realignment under Trump

Trump has frequently been described as an erratic president.1 Critics have often based this assessment on his trade policy. This impression was underlined by the never-ending succession of threats to impose tariffs, the withdrawal of threats, the introduction of tariffs, the suspension of tariffs, and the large number of exemptions and special regulations for individual companies. Trump, who described himself as a “tariff man”, publicly declared the reduction of trade deficits to be a top priority but remained far from achieving it. However, a closer look also reveals the extent to which the Trump administration embedded its trade policy in a foreign trade policy that was primarily geared towards the foreign and security policy goal of preventing China from becoming a super power. Under President Obama, US foreign policy had already begun to see China not only as an economic competitor, but also as a military rival for the first time. There is a great deal of continuity in this respect under President Biden.

The Trump administration took a new hard line against Beijing using a whole range of economic and diplomatic instruments.

The Trump administration took a new hard line against Beijing with a whole range of economic and diplomatic instruments. The NSS published in December 2017 identified China as the biggest geopolitical challenger, followed by Russia. In its NSS, the US government declared China to be a “revisionist power” and accused the country of undermining the international order.2 Trump’s trade policy advisor Peter Navarro stated in a frequently quoted speech to major US companies: “Economic security is national security”.3 In the president’s annually published trade strategies, the US Trade Representative and the White House made reference to the security threat posed by China’s aggressive economic and trade policy from 2017 onwards, which made countermeasures necessary.

As the academic literature on economic interdependence and the use of coercive instruments (economic statecraft) emphasises, one of the foreign and security policy priorities for the United States as a global power is to prevent or eliminate economic and technological dependencies on individual states. This applies in particular to a competitor and potential military rival such as China and concerns strategic areas such as communications technology.4 As argued in the economic statecraft literature, the United States can exclude strategic rivals when it controls access to an important network, such as in the global financial system (choke point effect). In this way, Washington secures a position of relative supremacy.5 The Trump administration openly and almost unreservedly used all available economic control instruments to expand US dominance in global networks, particularly vis-à-vis China, and to assert US interests. Both the Republicans and the Democrats supported the new course. This was reflected in several pieces of legislation that received bipartisan support in Congress. They concerned, for example, the rules of the Buy American Act (BAA), new export regulations and investment screening.

However, Trump’s aggressive economic policy did not stop at the interests of his own allies and close trading partners. In doing so, he damaged the United States’ foreign policy credibility beyond his presidency. In spring 2018, he imposed import tariffs on steel and aluminium, justifying them by citing a “threat to national security”. This was the first time a US government had declared that imports from close partners and allies also posed a threat to the United States. The Trump administration also dealt the WTO a blow from which it has still not recovered. The unilaterally imposed tariffs were a decisive overstepping of the bounds, as a “threat to national security” is only envisaged as a last resort under WTO rules. It is almost impossible for injured countries to provide evidence to the contrary and defend themselves against the tariffs. Subsequently, Washington blocked the reappointment of judges to the WTO Appellate Body, thus paralysing its dispute settlement mechanism.6

Overview of the trade policy instruments

During the election campaign, Trump declared that US trade deficits were a symptom of political weakness and made promises to impose tariffs. In the first trade strategy (The President’s Trade Agenda) of March 2017, the Trump administration signalled that it would use comprehensive trade instruments that went far beyond typical anti-dumping and the usual countervailing duties. A key objective in the document appeared to be the fight against trade deficits, paving the way for unilateral tariffs, even at the expense of allies and close partners. However, the focus of the Trade Agenda was on measures against China.

Section 201 duties (temporary relief)

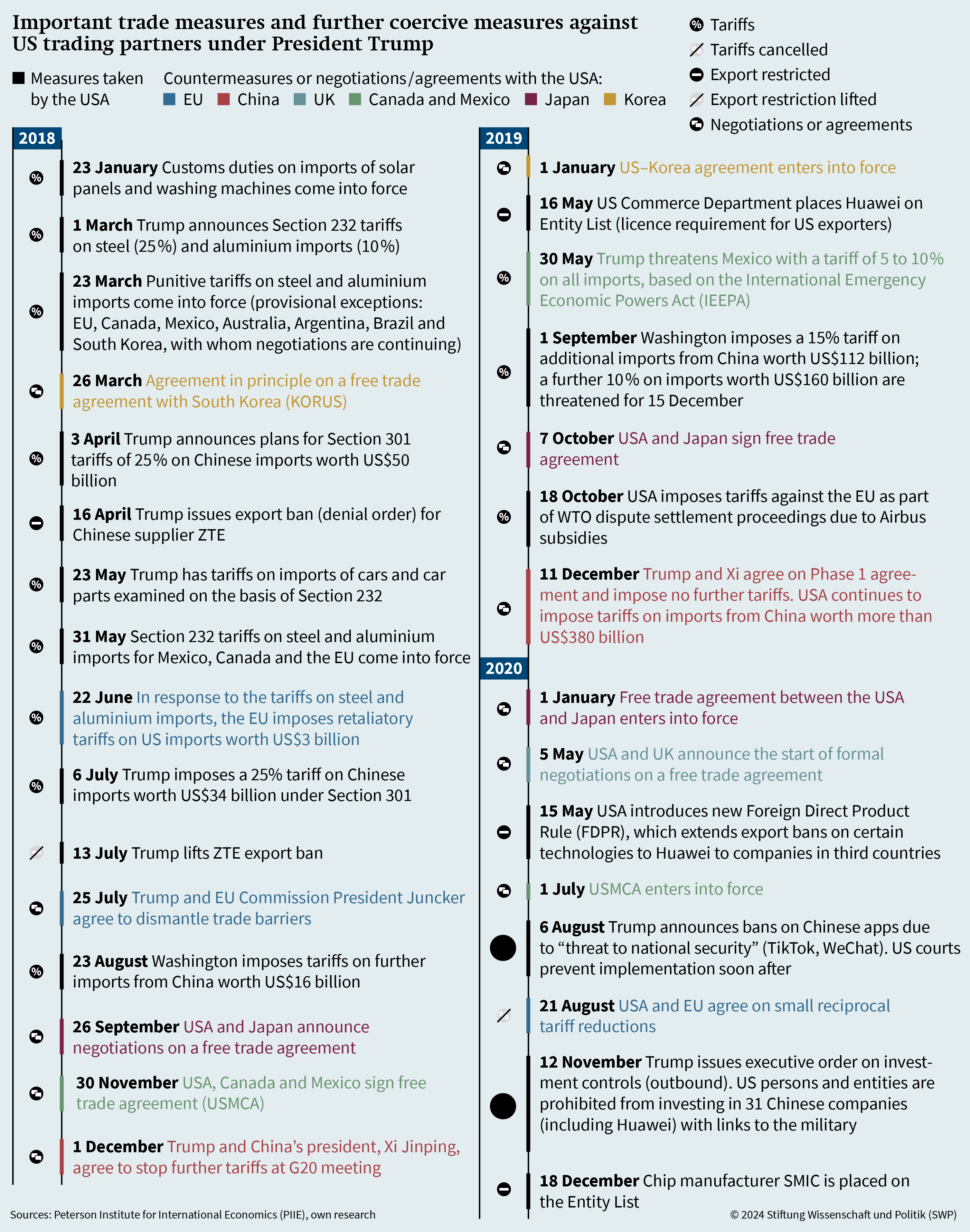

In February 2018, the Trump administration introduced new safeguard remedies on imports of solar panels and household washing machines from China and other countries for the first time. These tariffs were based on Section 201 of the US Trade Act of 1974. Overall, the volume of trade affected remained manageable. What was remarkable was the legal basis, which indicated a more aggressive course. Section 201 of the Trade Act allows Washington to protect US companies that come under so much competitive pressure due to increased imports that they are threatened with market exit. Companies can complain to the US International Trade Commission (ITC) about competitors. After review, the ITC can recommend tariffs or other measures to the president without having to submit a comprehensive report. Protective tariffs based on Section 201 are in line with WTO rules as long as they are imposed for a limited period of time – as in these cases for either three or four years.

The affected trading partners reacted with incomprehension but were unable to agree on a coordinated position, let alone a response. Taiwan and South Korea were the first countries to file a complaint with the WTO against the US tariff decision in January 2018. In response, China imposed its own tariffs on sorghum imports from the United States and also filed a complaint with the WTO. The EU declared its intention to respond “firmly and proportionately” to the US tariffs. In the end, Brussels filed a complaint with the WTO but refrained from taking its own tariff measures.7 In retrospect, the Section 201 tariffs appeared to be a “test balloon” for the responses of trading partners to protectionist US tariffs.

|

Figure 1

|

No united front was formed against Trump’s policy. Each trading partner was keen to agree individual tariff exemptions in bilateral talks, serving as an invitation to Trump to impose further tariffs.

Section 232 tariffs (national security threat)

On 1 March 2018, the Trump administration imposed tariffs of 25 per cent on steel imports and 10 per cent on aluminium imports. It justified this by declaring a “threat to national security” on the basis of Section 232 of the Trade Expansion Act of 1962. Trade measures under Section 232 are imposed without an expiry date.8 The statute gives the executive branch great flexibility to extend or suspend tariffs or allow exemptions.9 They impact individual countries with varying degrees of severity.10 Since China’s exports of steel and aluminium were already excluded from 95 per cent of the US market due to the Obama administration’s anti-dumping duties and other safeguard measures, the new tariffs under Section 232 did not represent a significant deterioration for Beijing. Nevertheless, the People’s Republic was the first country to retaliate – in April 2018, it imposed tariffs on US exports worth US$2.4 billion, roughly equivalent to the cost of the new tariffs on steel and aluminium. China also filed a complaint with the WTO – this time in parallel with the EU, Canada, India, Mexico, Norway, Russia, Switzerland and Turkey – which led to an investigation into the tariffs and countermeasures.

Trump’s decision led to a tariff escalation with the EU. Brussels imposed its own unilateral tariffs as “countervailing measures” without waiting for a WTO ruling. In May 2018, Trump instructed the US Department of Commerce to examine tariffs on cars and car parts on the basis of Section 232 and subsequently orchestrated the tariff dispute with the EU as a populist spectacle. Germany in particular then pushed for a compromise with Washington.11 In July 2018, then European Commission President Jean-Claude Juncker finally reached an agreement with Trump to drop further tariffs for the time being. Brussels also committed to purchasing a fixed quantity of agricultural products and liquefied natural gas (LNG) from the United States.

In May 2019, Trump declared a “national emergency” over close trading partner Mexico. He justified this by pointing to an alleged increase in the number of refugees at the southern border of the United States. Drawing on the International Emergency Economic Powers Act (IEEPA), Trump threatened a blanket import tariff of 5 per cent, which he later wanted to increase to 10 per cent. After Mexico’s parliament approved the free trade agreement with the United States and Canada (United States–Mexico–Canada Agreement, USMCA), Trump dropped his tariff threat. However, the move raised doubts among trading partners about the credibility of American statements on a threat to national security.

Section 301 tariffs (Intervention against unfair trade practices)

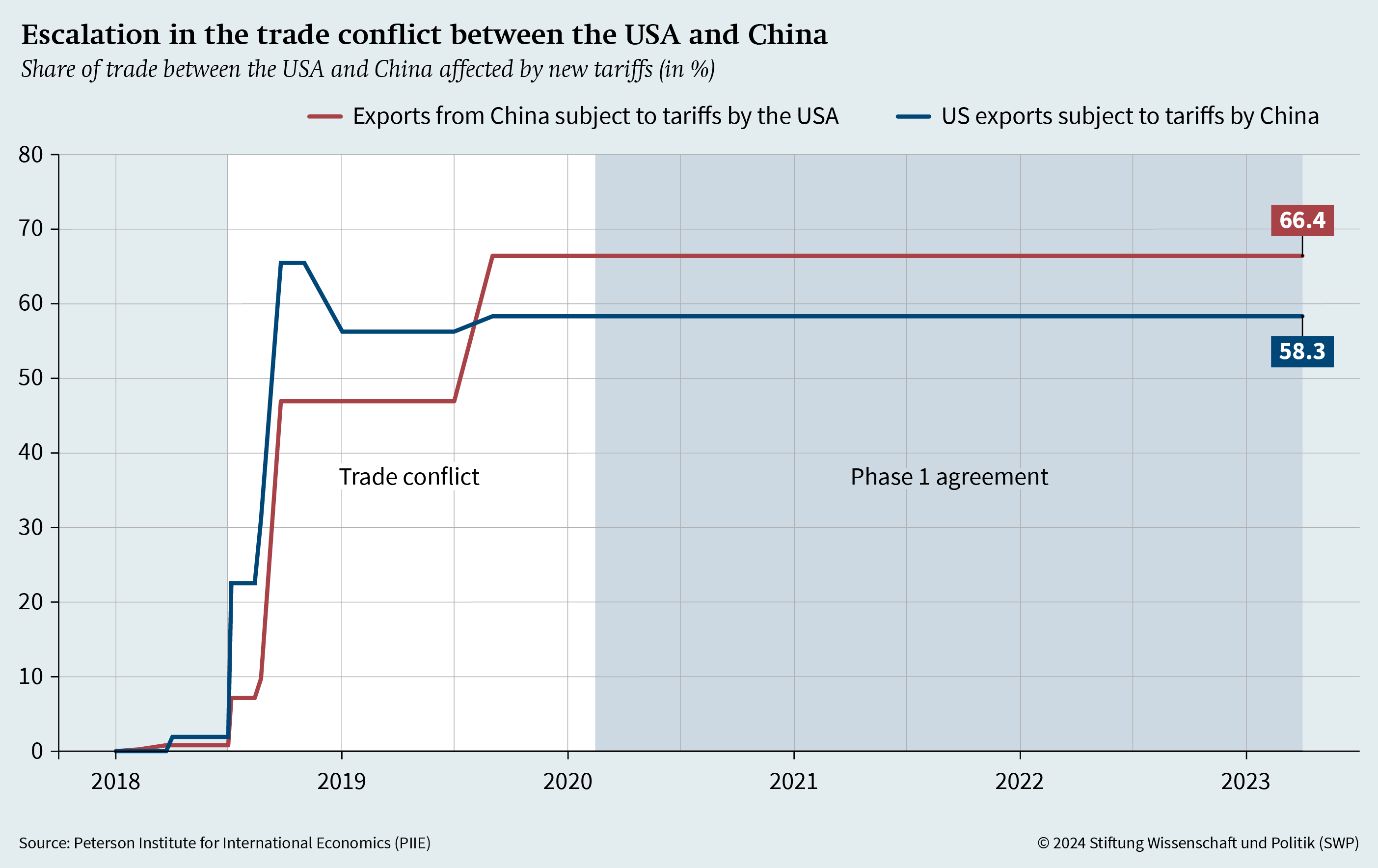

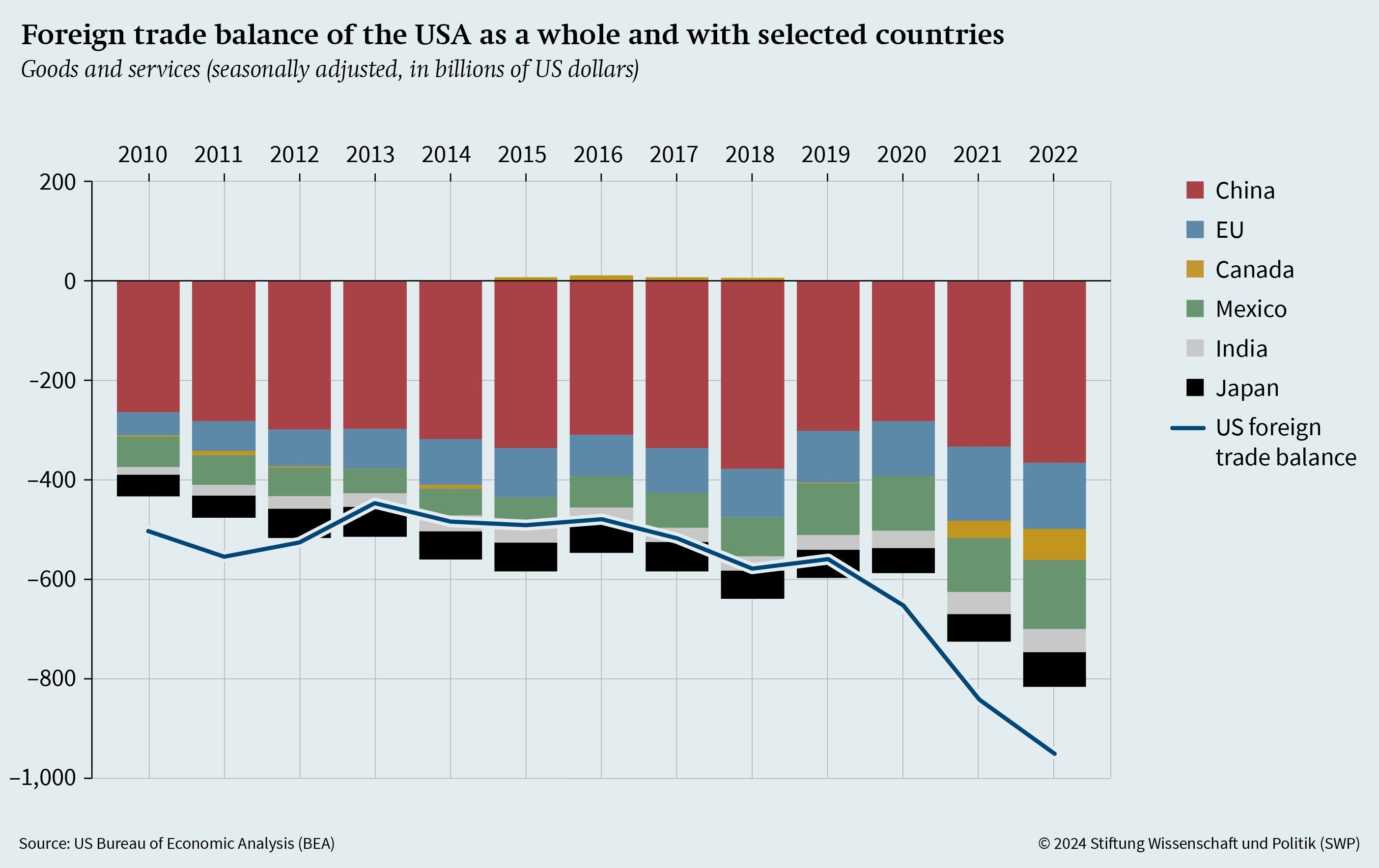

Trump used import tariffs based on Section 301 of the US Trade Act of 1974 as a key trade policy instrument against China. In August 2017 the Office of the United States Trade Representative (USTR), Robert Lighthizer, initiated an investigation under the statute into several allegedly “unjustified, unreasonable or discriminatory” trade practices carried out by the People’s Republic of China. Tariffs based on Section 301 are considered a particularly restrictive and effective trade policy weapon because they offer the possibility of taking direct, unilateral action without time restrictions against other countries in the event of an imminent infringement of intellectual property rights.12 The United States has rarely used this instrument since the WTO was founded.13 At the end of March 2018, the audit report on the Section 301 investigation was published, in which China was accused of “unfair trade practices” and systematic infringements of intellectual property rights against US companies. Lighthizer estimated the losses for US companies due to unfair Chinese trade practices to be US$50 billion annually.14 Based on the audit report, Trump imposed import duties of 10 and 25 per cent on 1,333 Chinese products in April 2018. This started a trade conflict between the two world powers that has still not been resolved (see Figure 2, p. 12). After several stages of escalation, presidents Trump and Xi Jinping agreed in December 2019 – as part of the “Phase 1 agreement” on balanced trade relations – to not introduce any new tariffs or increase existing tariffs. Trump waived further tariffs that had already been announced, which would have impacted almost all Chinese exports to the United States. However, the tariffs already imposed on around two-thirds of imports (by value of goods) from China remained in place. The US trade deficit then fell for a short time, mainly due to a decline in US imports from China. However, China’s exports of goods and the US deficit have now far exceeded the 2016 level (see Figure 3, p. 13).

Further coercive economic instruments vis-à-vis China

In addition to tariffs, Trump implemented a wide range of far-reaching, coercive economic and diplomatic measures, such as export and investment controls as well as sanctions and visa restrictions.15 They attracted less public attention than the tariff dispute, but they changed the course of trade more fundamentally and for longer than the tariffs, especially in the area of new technologies.

From 2018 onwards, the Trump administration increasingly targeted individual, particularly high-performing Chinese companies from those industries that Beijing itself described as strategically relevant in its Made-in-China 2025 strategy.16 The Executive Order on Securing the Information and Communications Technology and Services Supply Chain (EO 13873) of May 2019 signified a landmark measure by the Trump administration in the dispute over the control of communications technology. This order aimed to limit the risk of attacks on vulnerabilities in the information and communications technology supply chain. The Trump administration saw the involvement of Chinese companies in US telecommunications systems as a “risk to national security”, as they enable cyberattacks and industrial espionage. The order created a new legal basis that allowed Chinese companies ZTE and Huawei to be excluded from the sale of telecommunications equipment in the United States. Shortly afterwards, Trump banned all government and military personnel from purchasing or using communications technology from companies controlled by a “hostile” government, including ZTE and Huawei.

The US Congress also considered it necessary to take tougher action against Chinese companies. In response to China’s Made-in-China 2025 strategy, published in 2015, and its Military-Civil Fusion (MCF) programme, the US Congress tightened the regulations on exports of and investments in certain cutting-edge technologies.17 With broad bipartisan majorities, Congress passed two key pieces of legislation – the Export Control Reform Act (ECRA) and the Foreign Investment Risk Review Modernization Act (FIRRMA) – in August 2018.18 The laws codify US export and investment controls to address concerns regarding the release of critical technologies to end uses, end users and destinations of concern. The ECRA created a permanent statutory authority for the Export Administration Regulations (EAR). The EAR primarily control the export, re-export, and transfer of commercial, dual-use and less sensitive military items to end users, end uses and destinations of concern. They cover weapons technology, nuclear technology and certain toxic chemicals under the term “critical technology protection”. In addition, the ECRA introduced a new category of key technologies, the “emerging or foundational technologies”, which include areas such as biotechnology, AI, quantum computing, robotics and ultrasound technology. Although the ECRA and FIRRMA are general in nature, they developed into key pillars of the new, more robust economic policy approach to China.19

Export controls

|

|

|

Source: Chad P. Bown, US-China Trade War Tariffs: An Up-to-Date Chart (Washington, D.C.: Peterson Institute for International Economics [PIIE], 6 April 2023), https://www. piie.com/research/piie-charts/2019/us-china-trade-war-tariffs-date-chart. |

|

|

|

Source: Bureau of Economic Analysis (BEA), Data by Topic, International Trade & Investment, https://www.bea.gov/data/intl-trade-investment. |

Export controls in the Huawei and SMIC cases indicated a realignment of US strategy: The policy moved away from general and broadly effective rules to specific ones. The aim was to slow down China’s development in certain key areas. However, the export of goods and technologies in other areas was to be allowed in order to spare US companies enormous losses in sales.

Investment controls and financial sanctions

During Trump’s presidency, the United States also tightened its investment controls to prevent China from exerting influence and divesting critical technologies. Together with the ECRA, the US Congress passed FIRRMA with bipartisan majorities in August 2018.26 This act significantly expanded the review rights of CFIUS.27 The review procedures were updated and the budget of the inter-agency council was increased in order to be able to intensively review more investments.28 One of the most important innovations was the possibility for CFIUS to independently investigate planned takeovers of US companies without waiting for their notifications. In the case of investments in the areas of critical technology and critical infrastructure as well as the processing of sensitive personal data, the threshold for CFIUS to intervene has been lowered to include cases of a non-controlling investment. Being a majority shareholder is not necessary.29 The two laws, FIRRMA and ECRA, were intended to link the foreign trade policy instruments of investment and export controls more closely together. For companies whose exports must be licensed, an automatic review of foreign investments in the respective US companies is now required.30

The US investment review opens up the possibility of taking action against individual countries.

A central component of US investment screening is the ability to differentiate between countries. This allows controls to be targeted specifically at Chinese investments. According to FIRRMA, the Department of Commerce’s semi-annual reports to CFIUS and Congress should also explain the extent to which investments in US companies are linked to the Made-in-China 2025 strategy. In September 2017, Trump blocked the takeover of the Lattice Semiconductor Corporation by the Chinese investment firm Canyon Bridge Capital Partners. In March 2018, the government prohibited a further takeover attempt, as it was suspected that China was attempting to exert influence: Singapore-based chip manufacturer Broadcom had offered US$117 billion – the most expensive takeover bid in the technology sector at the time – to acquire a majority stake in US-based Qualcomm, the world’s fifth-largest semiconductor manufacturer.31 In both of these cases, Trump followed the recommendations of CFIUS and thwarted the takeover of companies, citing a threat to national security.

In quarters of the Trump administration, ideas ranged from state intervention in capital flows to controls on US investments made in China (outbound investment controls, OIC). However, there was resistance to this in the US Congress and in the financial industry. The originally planned OICs, which correspond to a government veto option for investments by US companies in other countries, were removed from FIRRMA.32 At the time, the majority of members of Congress considered additional investment controls to be too bureaucratic and feared competitive disadvantages for US companies.33

In the confrontation with China, Trump also used financial sanctions to deliver additional pinpricks to large companies, especially Huawei. For example, the Trump administration resorted to Iran-related sanctions. An arrest warrant issued by the US Department of Justice against Meng Wanzhou – the daughter of Huawei’s founder and the company’s CFO, who was charged with a serious violation of US sanctions against Iran – attracted a great deal of attention. The Chinese government interpreted this action as a tactic by Trump in the context of the bilateral trade conflict.34 He was also criticised in the United States for using financial sanctions as a bargaining chip in the customs dispute with China, thereby damaging the credibility of US sanctions policy.35 Under Trump, Congress itself played a significant role in the expansion of financial sanctions against China. With bipartisan majorities, Congress passed the Countering America’s Adversaries Through Sanctions Act (CAATSA) in July 2017, which contained new sanctions options based on human rights violations by state and non-state actors in other countries. The Trump administration used the new law to take action against China. It used reports of human rights violations by the Chinese government against the Uyghur population in Xinjiang province and the significant restriction of civil rights and freedoms in Hong Kong as an opportunity to impose targeted sanctions against Chinese leaders. As a consequence, the number of Chinese legal entities added to sanctions lists reached new records in 2017 and 2020.36

Biden’s Economic Policy Concepts

Biden ran for president in 2021 with the promise to fundamentally change foreign policy. He is committed to the principles of US foreign policy that have been in place since the Second World War, such as unwavering security guarantees for allies, whereas Trump disregarded them. However, as far as the relationship with China is concerned, Biden is continuing the course of his predecessor in many respects. His administration is also putting economic policy at the service of maintaining economic, technological and military superiority over China.

Biden is continuing his predecessor’s course towards China in many respects.

Biden’s economic policy programme – called “Bidenomics” by the media and ultimately by himself – rests on three pillars: 1. the alignment of foreign policy with the needs of the US middle class, 2. measures to protect economic security, which is understood as a part of the broader national security and 3. climate policy in the sense of a Green New Deal. During Biden’s term of office, China policy and measures to improve its own strategic position dominated the government’s political dealings. Other foreign policy goals such as global climate cooperation and other multilateral initiatives were repeatedly sidelined.

Foreign policy for the middle class

In preparation for a possible presidency, a team of authors at the Carnegie Endowment for International Peace published the “Foreign Policy for the Middle Class” strategy in September 2020.37 It is based on a study of the impact of US foreign policy since the end of the Cold War on the socio-economic positions of US citizens. The strategy aims to link security and economic policy more closely, as the bipartisan group of authors believes there was too much “silo thinking” in the two policy areas under previous Democratic and Republican administrations, which stood in the way of solving key problems.

“Foreign Policy for the Middle Class” sets out two overarching goals. The first is to align foreign policy with the interests of the US middle class.38 At the centre of foreign policy considerations, there should no longer be an aggregate national interest, as under previous Democratic and Republican administrations, as this often concealed the interests of the economically strongest and most influential groups. Instead, the next US government was to be measured by whether the middle class was benefitting from foreign policy decisions. The second overarching goal is to strengthen democracy as a form of government and social model, as it is increasingly competing with authoritarian political systems. The strategy emphasises the “outstanding role of the USA” as a superpower and hegemon that the US government must once again assume – for their own national interest and in order to support and preserve democracy as a form of government and social model. To this end, democracy must first be strengthened at home, which requires a greater focus on the needs of the US middle class. In “Foreign Policy for the Middle Class”, there is clear criticism of globalisation and the political pursuit of economic efficiency, which has disadvantaged certain groups of the US population. Profits from trade and global economic activities have not been sufficiently shared with the middle class. The strategy therefore contains two recommendations: First, sectors and regions that have suffered damage should be supported by the state. Next, foreign trade protection and coercive instruments should prevent unfair competition, and thus make labour and environmental rights more effective.

Economic stability, national security and competition with China

“Foreign Policy for the Middle Class” emphasises the importance of economic stability for the national security of the United States and its allies. The one-sided opening of the US market to foreign competition, particularly from China, has undermined economic stability. A new industrial policy should therefore strengthen domestic production and at the same time help the United States to become more independent from other countries and more resilient in times of crisis. To this end, US production should be supported by the state and, where necessary, completely rebuilt.

One focus in the strategy concerning the economic confrontation with China was placed on cutting-edge technology, as the authoritarian leadership in Beijing is striving for “economic and technological hegemony”.39 In order to halt China’s development into a technological superpower, the strategy envisages that a portion of defence spending will be redirected towards its own research and development (R&D) as well as the training of specialised workers. According to “Foreign Policy for the Middle Class”, the aim is to improve the United States’ innovative strength and long-term technological capabilities. In addition, the supply chains for critical goods are to be secured more effectively. The strategy also points out the costs and potential risks of an economic confrontation with China. Relocating industrial production to the United States could be accompanied by price increases, leading to higher economic costs. As the authors concluded, the US government should therefore prepare the middle class for negative consequences such as rising unemployment.40 At the same time, the government should respond to a middle class that wants its government to take more robust action against what is often perceived as unfair behaviour by Chinese companies subsidised by the Communist leadership. The US government should address unfair practices, such as theft of intellectual property and industrial espionage. US foreign policy should therefore focus on the immediate threats to the US economy. That includes that “(f)ree access to all important arteries of world trade” are defended.41 However, the strategy document also urges caution against an escalation in competition with China in order to prevent a conflict that could destabilise the economy and reduce prosperity.42

Green New Deal

In the 2020 election campaign, Biden adopted the climate policy agenda of the progressive wing of the Democrats, and thus the goals of the Green New Deal, and incorporated some key demands into his Build Back Better (BBB) programme.43 Biden did not go as far with his demands for spending on climate and environmental protection as presented in the original draft from the progressive wing of the Democrats in Congress. However, he adopted the approach of the party’s left wing and combined climate, labour and social policy in order to convince broader sections of the population about the benefits of climate policy measures. In coordination with those on the left of the party, Biden set himself three main goals for his presidency: 1. reducing greenhouse gas emissions, 2. making the necessary infrastructure investments for the transformation to renewable energy sources and 3. developing a globally oriented climate policy that is embedded in trade and foreign policy and relies on cooperation with other countries.

Biden’s plans included investments amounting to US$2 trillion. A large number of infrastructure measures were to be linked to the goal of climate neutrality (net zero greenhouse gas emissions by 2050). To this end, the production of renewable energy should be increased and grid expansion driven forward. According to the Clean Energy Plan published by the Biden team in September 2020, CO2 emissions from US buildings should be reduced by 50 per cent by 2035.44 Biden also announced extensive investments in the rail network and high-speed trains. His promise to ensure that 500,000 public charging stations for electric vehicles (EVs) are constructed by 2030, that electricity storage facilities are developed and that modern nuclear power plants are built also received a great deal of attention.45

Implementation of the Economic Policy Agenda

Security orientation of foreign trade policy

Shortly after Biden took office, the Interim National Security Strategy Guidance of March 2021 cast an initial spotlight on the Biden administration’s approach to security policy, which combines economic and security policy.46 The Guidance reflects the two overarching goals of the “Foreign Policy for the Middle Class” – strengthening the economic welfare of the middle class and democracy. As in the Trump administration’s 2017 NSS, the rise of China as a technological and military world power is seen as the greatest risk to US national security. Secretary of State Antony Blinken argued in his first keynote speech in March 2021 that China was “the only country with the economic, diplomatic, military, and technological power to seriously challenge the stable and open international system”.47 Blinken announced that the United States would compete with China where necessary and cooperate where possible. However, the relationship with China is “characterized by rivalry when it has to be”. In the detailed NSS, which was not published until October 2022 due to the outbreak of war in Ukraine, “economic security” is once again defined as part of “national security”.48 Almost a fifth of the security policy document is dedicated to economic policy measures.

Threats to national security also include theft of intellectual property and any attempt to undermine the United States’ technological leadership. The Biden administration announced early on that it was willing to use what it coined as “defensive” and “offensive” instruments. Accordingly, defence instruments include tariffs, export controls, investment screening and counterintelligence.49 It also announced a new industrial policy to serve as an “offensive instrument” to strengthen the US economy. On the one hand, this is intended to increase resistance to attacks from countries that rival the United States. On the other hand, it is intended to expand US supremacy in certain technology areas and promote the development of new technologies that are shared with allies and foreign policy partners.

As under Trump, the trade strategy and other plans for greater economic security, such as the supply chain review and legislative initiatives to implement the BBB agenda, have become building blocks of the NSS. In contrast to Trump, however, Biden sees climate change as an increasing risk to national security and at the same time as a “shared challenge” for countries worldwide. The Biden administration has stated that it believes that cooperation with other countries, including China, is needed in these areas.

A new industrial policy should eliminate dependencies on difficult trading partners in critical areas.

Against the backdrop of bottlenecks in critical supply chains during the Covid-19 pandemic and growing tensions with China, Biden initiated a series of comprehensive investigations into vulnerabilities in key US economic sectors after taking office. With Executive Order 14017 (America’s Supply Chains), the president commissioned a 100-day review of initially four priority product areas, namely semiconductors, large-capacity batteries, critical minerals and materials, and pharmaceuticals and active pharmaceutical ingredients.50 The review of the participating departments (Commerce, Energy, Defence, Health) was coordinated from the White House. The reviews of individual sectors were already available in July 2021. This was followed by investigations into six other sectors.51 Based on the reports, the Biden administration explained the areas in which it saw the US economy as being too dependent on difficult players and how supply chain resilience should be increased. The government described “resilient” as “a supply chain that recovers quickly from an unexpected event”.52 A new industrial policy was to completely eliminate dependencies on difficult trading partners, for example when it comes to microchips for military applications, and increase resilience in other areas. At the same time, jobs were to be created by bringing production back to the United States and expanding it.

New industrial policy

Biden began implementing the BBB agenda with an executive order (EO 14005) in January 2021, with which he tightened the application of the Buy American Act (BAA) of 1933.53 This law gives US suppliers priority when awarding public contracts. US products are to be given preference unless 1. a particular contract is incompatible with the public interest, 2. certain materials are not available or 3. a US authority certifies unduly high procurement costs.54 According to the BAA, for a product to be considered manufactured in the United States, at least 50 per cent of the production costs must be incurred there (domestic content requirement). Biden raised this figure to 75 per cent. In some areas, such as for iron and steel products, even higher US minimum percentages became mandatory under the regulation. In the case of construction materials, contract offers containing foreign products are to be automatically estimated as being 20–30 per cent more expensive in any cost comparison in order to secure an advantage for US suppliers. Biden combined the amended requirements on US shares in production with the requirement that all government contractors must undergo a Strategic Review of Supply Chain Sourcing.55 For the review, he had a Made in America Office set up as part of the important Office of Management and Budget under the White House umbrella.

An exemption from February 2023 concerns the BAA requirements for EV chargers. It allows the government to finance chargers made from foreign materials with the help of the Bipartisan Infrastructure Law, provided that the final assembly of these devices takes place in the United States. The exemption is intended to enable the establishment of a comprehensive network of charging stations for EVs, and thus help fulfil one of Biden’s most important promises from the last election campaign. Some in the US Congress, however, repeatedly tried to force the government to end the practice of such exemptions – several times at the expense of climate measures.

Infrastructure Investment and Jobs Act of 2021

The second step towards implementing the employee-centred agenda is the Infrastructure Investment and Jobs Act (IIJA), which was passed in Congress in November 2021 with large bipartisan majorities. It enshrined the previously tightened BAA clause.56 The Act provides for US$1.2 trillion to be spent on physical and digital infrastructure. The money is to be used primarily for the construction and expansion of roads, train lines, water pipes and high-speed internet connections. A significant portion of the budget is earmarked for road and bridge construction (US$110 billion) and airport modernisation (US$25 billion). However, Biden is also using the IIJA to implement a range of climate and environmental policy measures. These include spending on the rail network for passenger and freight transport (US$66 billion), the modernisation of energy infrastructure and grids (US$65 billion), water infrastructure (US$55 billion) and local public transport (US$39 billion). In addition, when the IIJA was passed, he promised to create around 1.5 million new jobs per year if the other components of the BBB agenda could also be implemented.57

Inflation Reduction Act of 2022

Biden was able to implement the centrepiece of his industrial policy, the BBB programme, in August 2022 with the Inflation Reduction Act (IRA). As the IRA was introduced as a regular budget bill, Biden only needed simple majorities in both houses of Congress for the vote – but only after difficult negotiations with the various Democratic party wings.

The Democrats lack the political majority to introduce a nationwide CO2 price.

The Biden administration has repeatedly emphasised the role of the IRA as a climate policy instrument when dealing with foreign policy partners. Immediately after taking office, Biden ensured that the United States returned to the Paris Agreement and is aiming for net-zero greenhouse gas emissions by 2050. According to the declaration on nationally determined contributions (NDCs) published shortly afterwards, CO2 emissions from the entire US economy are to be reduced by 50 to 52 per cent by 2030 compared to 2005 levels. Nevertheless, it was clear early on that Biden would not be able to rely on what most economists see as the most efficient way to reduce carbon emissions, a nation-wide carbon price. This was mainly due to a perceived lack of a political majority to introduce a nationwide CO2 price – as in the EU and individual US states. In addition, the Supreme Court set narrow legal limits for Biden’s climate and environmental policy ambitions with a ruling in June 2022. The president’s climate policy agenda was in danger of failing. With the IRA, Biden proposed an alternative path that consisted of reducing CO2 emissions with the help of a mixture of economic incentives and binding targets and timetables.

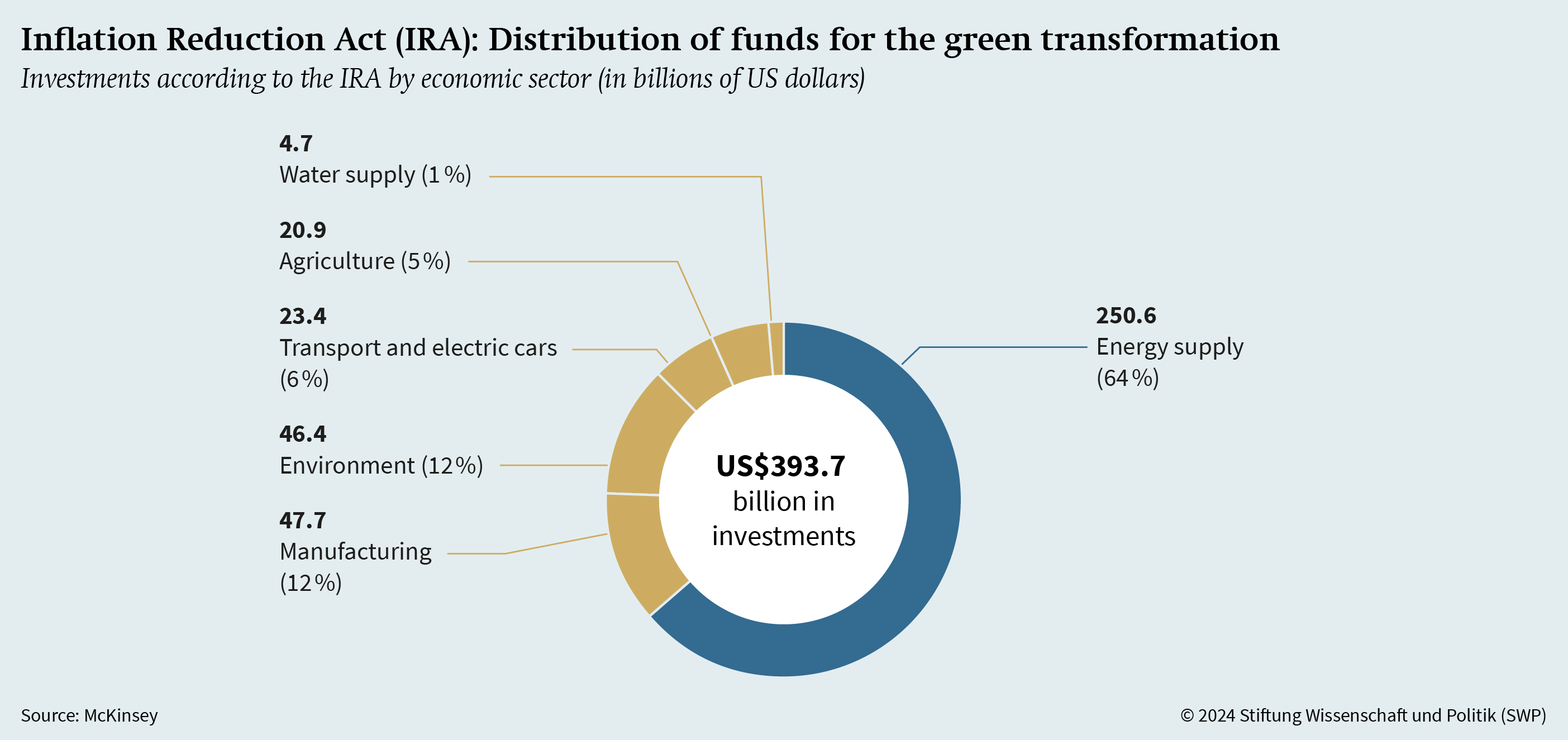

According to Biden-administration estimates, the law was to direct around US$369 billion of federal funding over 10 years to clean energy and other climate protection measures as well as around US$64 billion for additional spending on statutory healthcare through the Affordable Care Act. At the same time, the Biden administration pledged to reduce the US budget deficit by US$300 billion by the end of 2031. To this end, it introduced a new minimum tax of 15 per cent for large US and foreign companies. The climate protection funds were to be delivered through a mix of tax incentives, grants and loan guarantees. In the initial planning, clean electricity and transmission command the biggest slice, followed by clean transport, including EV incentives. The fact that the majority of energy and climate funding is in the form of uncapped tax credits has made it difficult to predict the actual costs of the IRA tax incentives. In addition to climate policy considerations, the decision to provide uncapped EV tax credits was taken with the strategic aim of establishing the highest value-added segment of EV production – namely batteries and motors – in the United States. Starting in 2023, qualifying EVs became eligible for a tax credit of up to US$7,500 and 4,000 for new and used vehicles, respectively. Qualifying home improvements became eligible for a tax credit of up to 30 per cent of the total cost, capped at US$1,200 per year. A year after the IRA was introduced, one financial industry report estimated that for all EV credits alone, costs could rise to as much as US$390 billion over the decade, more than 27 times more than the original estimated cost.58 Early in 2024 the Congressional budget stated that it now estimates the total cost of the climate provisions to be at least twice as much as initially projected, close to US$750 billion for the period from 2022 to 2031.59

|

Figure 4

|

|

Source: Justin Badlam et al., The Inflation Reduction Act: Here’s What’s in It (New York, NY: McKinsey & Company, 24 October 2022), https://www.mckinsey.com/industries/public-sector/our-insights/the-inflation-reduction-act-heres-whats-in-it. |

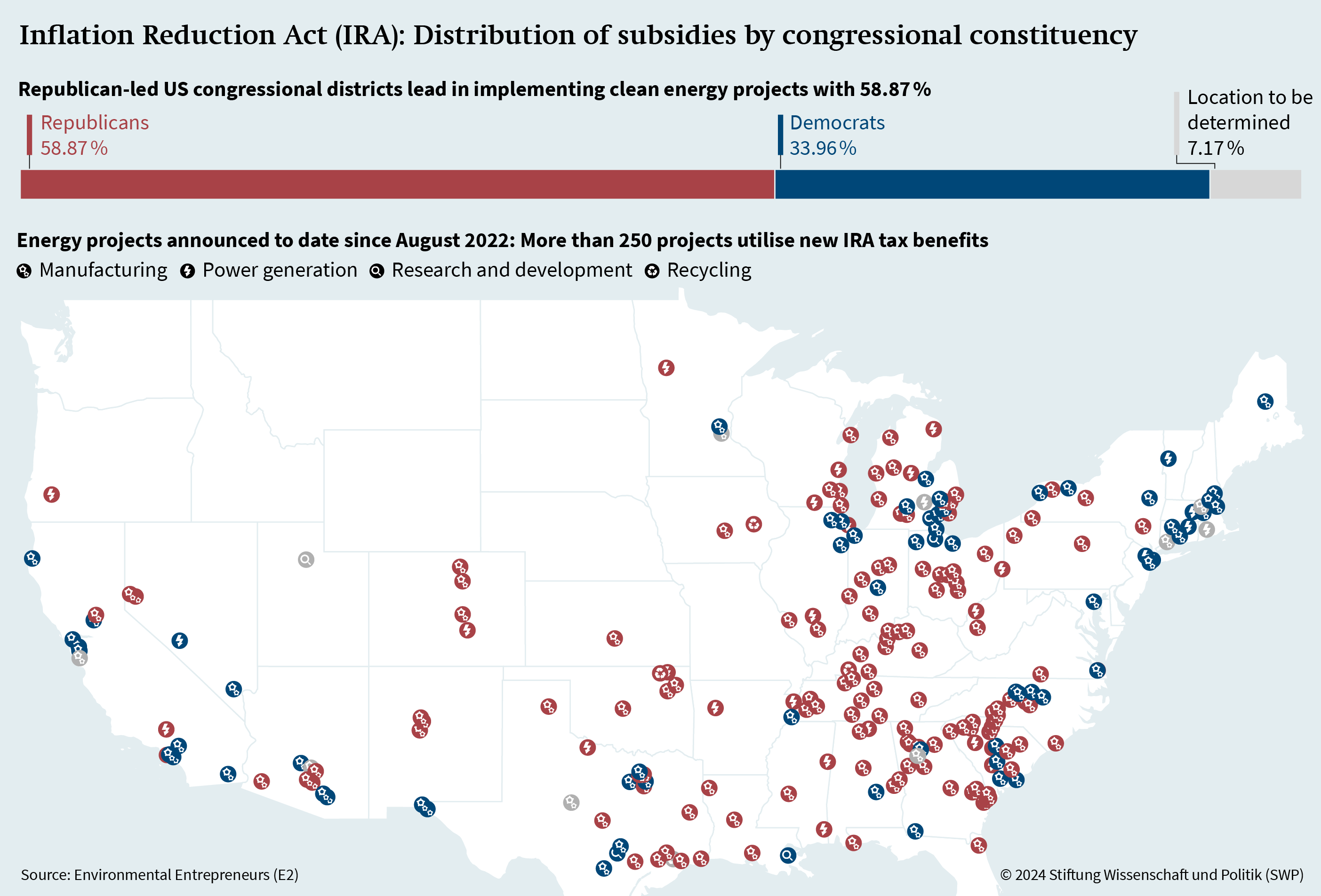

Although US trading partners welcome the climate policy impact of the IRA, they criticise the extensive exclusion of foreign producers from subsidies and tax credits. This results from the provisions of the law on the use of US components (local content requirements).61 As trading partners in the USMCA, Canada and Mexico have succeeded in obtaining exemptions for their own producers, who can therefore benefit from US subsidies and tax credits. Japan, South Korea and the United Kingdom have now also been granted free access to subsidies as partners in US free trade agreements or through special agreements. In contrast, the EU, which has no free trade agreement and no special agreement with the United States to date, considers itself disadvantaged by the exclusion of US subsidies.

|

Figure 5

|

|

Source: Environmental Entrepreneurs (E2), Clean Energy Works, https://e2.org/announcements/. |

Despite all the criticism of the IRA from Europe, it should not be forgotten that the Biden administration has already accommodated the EU in two areas. First, the US Treasury Department, which is responsible for tax credits, has made it clear that manufacturers from the EU can fully benefit from tax credits for exports of commercial vehicles. Second, the Biden administration had already adjusted its plans in the run-up to the IRA so that European vehicle manufacturers producing in the United States would benefit. In the original draft bill, only manufacturers with a unionised workforce were to receive government support. This would have affected German manufacturers producing in the southern US states with a non-unionised workforce. However, the rule was dropped, partly due to pressure from USMCA trading partners Canada and Mexico.

The EU remains concerned about the (short-term) fall in production costs in the United States as a result of the IRA.63 Brussels fears a relocation of new investments to the United States, which could have a negative impact on production in Europe in the long term. The public promotion of certain goods along the entire production chain – including the extraction and processing of individual minerals in the manufacture of batteries – could contribute to this. The decisive factor for the relocation of entire factories is likely to be the combination of two factors: 1. the rise in energy prices due to the restructuring of energy markets following the Russian attack on Ukraine, and 2. subsidies in the United States and other countries. In the long term, a relocation of R&D to the United States would be particularly detrimental to the innovative strength of European companies. However, whether the IRA will lead to an outflow of R&D from Europe to the United States remains to be seen. The fact that subsidies under the IRA are predominantly used to expand existing “green” technologies and not for experimental technologies still under development speaks against a relocation of this area.64

CHIPS and Science Act of 2022

The CHIPS and Science Act was the Biden administration’s response to the US economy’s high dependence on semiconductor chips, particularly from Asia. It sees this as a significant risk to national security. For years, there has been growing concern in the United States that supply chains for this technology, which is relevant to all areas of the economy, could break down. There are even doubts as to whether the demand for secure US-made semiconductor chips for the military can be adequately met. Due to geo-economic tensions in the region, as well as potential problems such as natural disasters, US studies have been urging a greater diversification of production for several years and recommending that capacities be re-shored to and expanded in the United States.65

The CHIPS and Science Act, for which Biden received bipartisan majorities in Congress in July 2022, provides for more than US$50 billion in public funding over 10 years. The funds are to be made available for the construction and further development of production facilities for semiconductor technology (US$39 billion), for R&D and for training measures in the STEM sector (US$11 billion). The law prioritises the production of the most modern and technically sophisticated semiconductors, for which around US$28 billion of the US$39 billion in public funding is earmarked. Funding applications in the area of particularly high-performance new “leading edge” semiconductors are to be brought forward. However, the US government is also providing around US$10 billion in funding for the manufacture of the current generation of semiconductors, which are used in many economic sectors and in the military. Reliance on China for less powerful chips is also to be reduced. To this end, the production of such chips, among other things, is to be established in allied countries.

The – at first glance relatively low – public spending is intended to stimulate further private investment. The Biden administration has earmarked up to US$6 billion for loans and loan guarantees for the years 2022 to 2026 to facilitate up to US$75 billion in private investment. The law also creates the basis for the approval of up to US$24 billion in tax credits for the construction of chip production facilities by January 2027. Companies can get up to 25 per cent of the investment back as a tax credit. According to the industry, private companies already invested more than US$200 billion in semiconductor production in 20 US states in the first year.66

Coercive measures against China

Like Trump, Biden is also focusing on economic unbundling and coercive instruments (economic statecraft) vis-à-vis China. The focus so far has been on critical technologies such as semiconductors, supercomputers and AI applications. In implementing its measures, the Biden administration is applying the “small yard, high fence” approach.67 The United States, together with its allies, still has control over certain critical technologies, such as the most modern and powerful semiconductors, AI applications and high-performance computers that can be used for both civilian and military purposes. Biden is trying to exclude China from this with a particularly “high fence”.

Continuation of punitive tariffs

After taking office, the Biden administration was faced with the question of whether to continue Trump’s tariff policy towards China. The assessment of China’s “unfair trade practices” did not change under Biden. Some US companies openly criticised the comprehensive Section 301 tariffs after Trump’s election. The critics mainly came from sectors of the economy that rely on Chinese imports. Nevertheless, it is unclear whether and under what conditions Washington would be prepared to reduce them.

In Congress, Biden received bipartisan support for unilateral tariffs.

Whether the punitive tariffs are compatible with WTO rules still played no role for the Biden administration. On the other hand, a dispute arose within the government over the impact of the tariffs on inflation, which rose to more than 8 per cent in 2022. Some departments, most notably the Treasury Department, had spoken out in favour of lowering tariffs in order to avoid further price increases and curb inflation. However, those in the administration who wanted to retain Section 301 tariffs as political leverage against Beijing prevailed. In September 2022, the USTR declared that it would maintain the tariffs at the request of US companies that would be harmed by the dismantling of the tariffs. The decision also came as a surprise because the review process carried out by the USTR in which affected companies have their say, had not yet been completed.68

In general, the level of tariffs varied from 7.5 per cent on many consumer goods to 25 per cent on vehicles, industrial components, semiconductors and other electronics. Biden allowed exemptions to relieve the burden on individual US companies. The most important of the 352 import categories that the president exempted from import duties include cell phones, laptops and video game consoles from China. In May 2024, the USTR announced that it had completed its long-awaited full review of the Section 301 tariffs on Chinese imports. Shortly after, president Biden declared he would continue the existing tariffs on Chinese-origin goods imposed by the Trump administration. At the same time, the Biden administration proposed to significantly increase the Section 301 tariff rates to 100 per cent on imports of China-made EVs (from 25 per cent), 25 per cent on EV battery parts (from 7.5 per cent) and to 50 per cent on both solar cells and semi-conductors (from 25 per cent each). Additional tariff increases in a range of other product categories were also proposed.69 In order to mitigate the negative consequences of the tariffs, the USTR first extended previously approved exemptions until the end of 2023. The USTR is now inviting public comments on the manufacturing equipment that should be exempt from the Section 301 duties. However, as US observers have noticed, it appears that the Biden administration is only willing to consider tariff exclusions that specifically benefit 19 types of solar manufacturing equipment, despite requests to do so from many US importers and some members of Congress to allow for broader tariff exemptions.

At the same time, the Biden administration is also retaining the tariffs that Trump imposed on the basis of Section 201 of the Trade Act. Although the tariffs on imports of Chinese solar cells and modules are a burden on the US solar industry and run counter to Biden’s climate policy goals, he has extended the protective tariffs on solar cells until 2026. Until recently, Biden has continued to grant tariff exemptions for certain solar cells from China that are essential to the energy transition. He also suspended the protective tariffs on imports of solar modules and cells from Cambodia, Malaysia, Thailand and Vietnam until June 2024, although investigations commissioned by the government had shown that imports from these countries contain a significant proportion of Chinese products and violate US protection rules.70 In his May 2024 tariff announcement, Biden included his plan to imminently remove this exclusion as a step to assist US-based solar manufacturers supported by the IRA and to provide “tariff protection from unfair imports”.

In Congress, Biden received bipartisan support for the unilateral tariffs. In the House of Representatives, a Democratic majority opposed dismantling the China tariffs. Under the Republican majority, the anti-China stance continued after November 2022. Regardless of the political majority, little opposition to tariffs on China is expected in the next US Congress. However, Congress repeatedly pushed for new trade restrictions and further coercive measures against China. In December 2021, it passed the Uyghur Forced Labor Prevention Act (UFLPA).71 The law is intended to prevent imports of goods that were produced in whole or in part under conditions of forced labour in the People’s Republic of China or even only partially processed there, especially in the Xinjiang Autonomous Region. It also includes a mandate for the US government to negotiate equivalent measures with allies and foreign policy partners to prevent US companies from unilaterally bearing the costs of coercive measures. The simultaneous implementation of these two elements of the UFLPA would come close to placing an international embargo on Chinese textiles.

Export controls

Export controls also play a central role in the strategic approach towards China under Biden. Unlike Trump, Biden has declared that he is not aiming for a comprehensive decoupling from China. However, his administration is continuing the export controls initiated by Trump in order to promote a narrowly defined technology decoupling. The focus is on critical technologies that serve both purely commercial and military purposes and can secure a decisive advantage over potential military rivals.72 By reviewing supply chains in its first year in office, the Biden administration has been able to gain a good picture of where its own dependencies on China lie, but also of the choke points at which Washington, together with military allies and close partners, has control over relevant technologies. In response to Russia’s attack on Ukraine in February 2022, Biden applied export controls as part of the sanctions measures to deny Russia’s army and industry access to Western cutting-edge technology. Washington initially announced that it would also oblige third countries to implement US export controls via a Foreign Direct Product Rule (FDPR). After the EU and other US partners agreed to introduce comparable measures as part of a sanctions coalition of 39 countries, Washington suspended the FDPR for these countries.

In the NSS of October 2022, dealing with China is named as the most important foreign and security policy priority. As National Security Advisor Jake Sullivan explained, the United States is pursuing the goal of gaining the “greatest possible advantage” over China with the new export controls. According to Sullivan, the United States and its allies have learnt an essential lesson from the use of controls against Russia: “Technology export controls can be more than just a preventative tool [...] they can be a new strategic advantage in the toolkit of the United States and its allies to impose costs on adversaries” and “weaken their capabilities on the battlefield”.73 With the executive orders of 7 October 2022, the Biden administration introduced a licensing requirement for the export of semiconductor chips to China. The focus is on chips used for supercomputers and AI.74 The BIS also prohibits the export to China of manufacturing equipment for particularly powerful chips and tools for their production. Furthermore, AI applications and supercomputers may only be exported to China with a licence. The BIS is endeavouring to curb China’s military capabilities, especially weapons of mass destruction. Washington is also trying to prevent AI from increasingly being used for military purposes and citizens from being comprehensively monitored, including human rights violations.

The Biden administration also linked an FDPR to its own measures, but continued to strive for a unified stance towards China. More than 40 per cent of the manufacturing machines and tools (including software) produced worldwide for high-performance semiconductor chips are developed and produced in the United States. The remaining production is concentrated in companies in Japan and the Netherlands. In spring 2023, the United States therefore agreed with these two countries on export controls for semiconductor manufacturing equipment. Since then, similar regulations have applied to companies such as Nikon Corp, Tokyo Electron and ASML, the toughest competitors of US manufacturers.75 In March 2024 there were rumours about a US push to get Germany and South Korea to introduce export controls on certain lenses and potentially lasers and chemicals used in ASML chipmaking machines.76

Chinese institutions subject to export controls also continued to obtain high-performance chips.

Reports from the summer of 2023 indicate that Chinese entities on export control lists were still able to obtain high-performance chips. Access to these apparently involves a combination of smuggling via neighbouring countries, rental agreements with non-sanctioned companies that provide certain high-performance chips on an hourly basis, and virtual use of the services of cloud computing companies in the United States.77 Just over a year after the original regulations were published, the BIS tightened the rules. In October 2023, Washington expanded the list of regulated goods and also those countries to which exports of certain semiconductors are only permitted with reservations. However, the rules do not (yet) cover the rental of chips. BIS asked companies to suggest solutions to this problem.78 On the one hand, this example demonstrates the difficulty for the government in forcing US companies to implement legally complex technology controls. On the other hand, it underlines the need for Washington to work more closely with other countries to make it more difficult to circumvent the rules.

Investment controls and financial sanctions

In the autumn of 2021, the Biden administration issued an executive order to further tighten the rules for investment screening.79 The Committee on Foreign Investment in the United States (CFIUS) is to focus primarily on investment risks in the area of new technologies still under development (evolving and emerging risks). Particular attention is to be paid to investment trends in certain sectors and the resilience of supply chains. In the case of planned investments in US companies, the precautions for cyber security, energy security and infrastructure as well as for securing large data sets with personal information should also be examined.

With Executive Order 14105, dated 9 August 2023, Biden established a targeted outbound investment programme, including restrictions on US investments in “countries of concern” (outbound investment controls, OICs) for the first time.80 Currently, only China – including Hong Kong and Macau – fall under this definition. The OICs are intended to establish reporting obligations for investments in certain narrowly defined technology sectors that have not yet been finalised. With the Order, the president instructed the US Treasury Department to develop precise rules. In a statement in May 2024 before the House of Representatives, Commerce Secretary Gina Raimondo declared that the Commerce Department was working closely with the Treasury Department on investment controls on high-performance semiconductors and microelectronics, quantum computing information technologies and certain AI systems. It expects to issue final rules by the end of the year.81

Restrictions on investments in the above-mentioned areas of technology – to which certain green technologies, biotechnologies and ultrasound technology could be added – have been under discussion for some time.82 Several bills are currently circulating in the House of Representatives that could permanently enshrine OICs. Proposals have included notification requirements, prohibitions of investment in certain sectors and a case-by-case review. They differ with regard to relevant countries, sectors and activities to be covered. While most legislation targets China, some proposals include Iran, North Korea and Russia. Some include directions for the US government to work together with other governments to implement similar rules to minimise negative impacts on US firms.83 So far, none of the proposed legislation has won a majority in either house of Congress. Clearly, there are concerns in Congress about government intervention in the capital markets. US industry associations are opposed to OICs, as they fear retaliatory measures by China that could affect not only the financial sector but also other areas of the US economy.84 Some critics of new capital market restrictions on China argue that existing sanctions should be fully utilised instead of complicated and potentially difficult-to-implement OICs.

In its first year in office, the Biden administration reviewed all of the US Treasury Department’s sanctions programmes. It also continued its course vis-à-vis China in this area and restructured procedures where necessary. Biden transferred responsibility for the sanctions list created by Trump for companies in the Chinese military-industrial complex (Chinese Military-Industrial Complex Companies List, CMIC) from the Department of Defence to the Department of the Treasury. In general, Biden imposed roughly the same number of sanctions against Chinese legal entities (individuals, companies and other entities) as Trump.85 Like his predecessor, Biden also imposed sanctions against Chinese individuals, most frequently for violations of sanctions regimes that actually apply to third countries such as Iran. Like Trump, Biden also used the CMIC list to impose sanctions due to “repression and serious human rights violations”. For example, companies that work with Chinese military and security authorities and use surveillance technology against the population were listed. If a Chinese legal entity is suspected of using certain technologies such as high-performance semiconductors, AI applications or quantum computers for the purposes of surveillance that violates human rights or for warfare, the US Treasury Department can already prohibit capital transactions between the listed persons and US companies.

Reluctant trade policy

As the Biden administration places the highest priority on strengthening the domestic economy and strategic positioning vis-à-vis China, trade policy initiatives have taken a back seat. Neither Biden nor Trade Representative Katherine Tai commented on the possibility of resuming negotiations on a transatlantic free trade agreement (Transatlantic Trade and Investment Partnership, TTIP) with the EU, which were already well advanced under President Obama. A return by the United States to the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) remains out of the question. In contrast, the USTR opened a series of trade initiatives, known as economic frameworks, starting in mid-2021, which differ in structure and content from traditional free trade agreements. From the outset the Biden administration ruled out negotiations on improved market access, which were common in previous free trade agreements. From a US perspective, the most important frameworks are the Indo-Pacific Economic Framework (IPEF) and the Trade and Technology Council (TTC) with the EU. These were joined shortly afterwards by economic dialogues with Central and South American countries (Americas Partnership for Economic Prosperity, APEP) and talks with African trading partners on continued preferential market access (African Growth and Opportunity Act, AGOA).

EU-US Trade and Technology Council (TTC)

Immediately after Biden’s election victory in November 2020, the EU sought to revitalise transatlantic trade cooperation. Brussels also wanted to talk to Washington about how the two sides could combine climate and trade policy. The Biden administration pushed for common standards to be agreed with Europe for the use of new technologies. After the European Commission proposed a new dialog format at the highest political level in early December 2020, Washington and Brussels agreed to establish a Trade and Technology Council (TTC) in the summer of 2021. Some of Biden’s trade policy decisions in the run-up to this had contributed significantly to improving the transatlantic relationship. The new president suspended the Section 301 tariffs that Trump had imposed as punishment for the plans of some European countries to introduce digital taxes. With regard to the Section 232 tariffs on steel and aluminium imports from the EU, Biden accommodated European Commission President Ursula von der Leyen with tariff rate quotas. The EU and United States also agreed to work out a solution for the duty-free import of “green” steel and aluminium. Both sides described the temporary suspension of tariffs as a new beginning.86 Biden and von der Leyen reached a similar compromise in the dispute over subsidies for aircraft manufacturers Airbus and Boeing; the dispute had already lasted almost 17 years by that point and had resulted in a cascade of reciprocal punitive tariffs.87 The United States and the EU suspended their tariffs for five years. They also set up a working group to formulate a legal compromise by mid-July 2026.88

For some time before the first TTC in Pittsburgh in September 2021, it was unclear which topics should be discussed within the framework and which should be outsourced to other forums. Brussels called for a wider range of topics beyond technology policy. The EU also tried to dispel the impression that it was letting the United States impose an anti-China dialog on it. After the diplomatic crisis in connection with the AUKUS submarine agreement almost caused the first TTC to collapse, both sides expressed their satisfaction with the agreed transatlantic work plan at the end of the meeting.89 In the 17-page final document from Pittsburgh, they agreed on 10 thematically defined working groups, ranging from specific issues in the area of supply chains to major projects such as the fight against corruption, setting standards for AI and reforming the world trade order.90 However, some pressing problems that initially strained the transatlantic relationship were excluded from the TTC. Energy issues were shifted to the EU-US Energy Council, which had been established in 2009. Following the negative ruling by the European Court of Justice against the Privacy Shield agreement, a new EU-US Joint Technology Competition Policy Dialogue was set up to deal with a successor agreement on secure data transfer. The regulation of digital companies with a monopoly position and the EU’s plans at the time for the Digital Markets Act (DMA), which came into force in November 2022, were also to be discussed there.

Russia’s attack on Ukraine rapidly changed economic policy cooperation between the EU and the United States.

Initially, the EU states remained cautious about the prospects of success of economic talks with the United States. However, Russia’s attack on Ukraine in February 2022 changed their cooperation in a very short space of time. As both sides emphasised, the TTC made it possible to quickly and pragmatically coordinate comprehensive economic sanctions against Russia. The EU achieved a decisive diplomatic success when Washington recognised European export controls and suspended the already enacted FDPR against EU states.

After four meetings, the TTC has produced further concrete results. These include an Artificial Intelligence Code of Conduct, which deals with the trustworthiness of AI and contains starting points for a joint approach. A task force has been set up for the field of quantum computer technology to ensure that research projects on both sides have access to research funding. In addition, a joint working plan for sustainable trade (Transatlantic Initiative on Sustainable Trade, TIST) is being developed. In contrast, the two sides were hardly able to come any closer to an agreement with regard to linking trade and climate policy in multilateral organisations as well as reforming the WTO and reviving the second instance of its dispute settlement mechanism (Appellate Body). New US subsidies within the framework of the IRA as well as subsidies and the Carbon Border Adjustment Mechanism (CBAM) on the part of the EU continue to give rise to discussions about fair competition between the transatlantic partners. Looking ahead to future TTC meetings after the European Parliament and the US presidential and congressional elections in autumn 2024, it remains to be seen whether the TTC would allow for closer cooperation on measures against coercive or market-distorting Chinese trade practices, as well as measures to control dual-use goods, such as export and investment controls. Some member states, including Germany, have voiced concerns about Biden’s recent decision to place tariffs on imports of China-made EVs of 100 per cent and to significantly raise tariffs on other products under Section 301 of the US Trade Act. At the same time, European Commission President von der Leyen said, “The world cannot absorb China’s surplus production”.91 Under her presidency, the European Commission is building a case for countervailing duties under WTO rules, suggesting that the EU is also likely to take a tougher stance to counter Chinese overproduction but is following a different approach than the US government. Despite continuing differences of opinion, the TTC has created a transatlantic framework that could promote a balance of interests, and thus closer cooperation in future, even without a transatlantic agreement on trade and investment.

Indo-Pacific Economic Framework for Prosperity (IPEF)